You May Also Like:

-

Five Trends Australian Property Investors Must Watch in 2026

-

How Will Brisbane Infrastructure Kickstart the Property Market?

RBA’s Decision Predictions

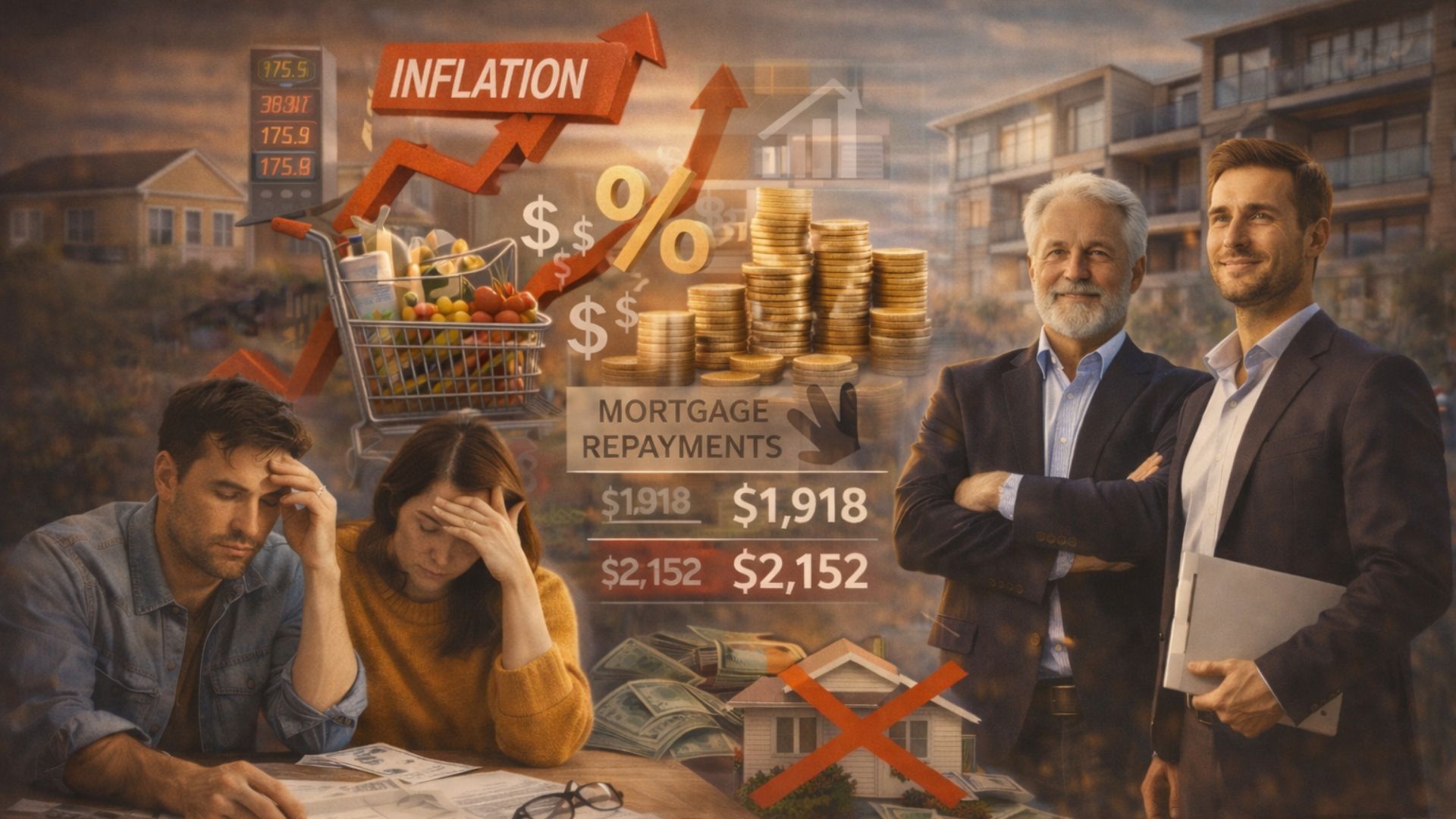

Australia’s latest inflation figures have reignited debates about whether the Reserve Bank of Australia (RBA) will increase the cash rate at their first meeting of 2026. For property investors, homeowners and aspiring first-home buyers, the RBA’s decision will have real implications for borrowing costs, housing affordability, property values and the broader strength of Australia’s residential real estate markets.

For buyers trying to understand how inflation and interest rates may affect their purchase plans, working with a buyers agent Brisbane can help clarify borrowing capacity, suburb selection, and market timing.

Why Did Inflation Surprise the Market in Late 2025?

When the Australian Bureau of Statistics (ABS) reported in late January 2026 that headline inflation — as measured by the Consumer Price Index (CPI) — had risen to 3.8% over the year to December 2025, it was higher than most economists expected and clearly above the RBA’s long-run target band of 2–3%.

This left a lot of uncertainty around cash rates, interest rates, and whether the expected 2026 interest rate drops would actually come into fruition.

Crucially, inflation pressures are not limited to volatile components like energy, fuel, groceries, and increases in other living expenses. Housing costs, including rents and the prices of owner-occupied dwellings, were among the largest contributors, rising by around 5.5% over the same period.

Food prices, transport and recreational services also climbed significantly.

Even the RBA’s preferred measure of underlying inflation, the trimmed mean CPI, which strips out the most volatile price changes, has crept above its expected levels, signalling that price pressures are broadening across Australia’s economic environment.

Why Do These Inflation Numbers Matter to the RBA?

The RBA’s mandate is to maintain price stability, supporting economic growth while keeping inflation within a target band of 2–3% over time.

When inflation consistently sits outside this range, the central bank typically adjusts monetary policy to steer it back toward target.

When inflation is above 3%, it places pressure on the RBA to increase the cash rate to slow spending, and re-align the inflation rate back within the target range.

This report of increased inflation has surprised economists because for much of 2025, inflation showed signs of moderating, prompting hopes among borrowers that interest rates had peaked and we would be seeing cuts to interest rates as soon as early 2026.

However, this unexpected uptick in the December inflation data has shifted this narrative. Several major banks and economic observers now see a moderate rate rise, likely around 25 basis points, as a real possibility at the RBA’s first policy meeting of 2026 in early February.

This potential hike would follow recent rate cuts in 2025 and would signal that the central bank is no longer confident inflation will drift back into the target range on its own.

What Would a Rate Hike Mean for Property Values?

The relationship between inflation, interest rates and property prices are complex, but there are some powerful dynamics that every property investor should understand.

How Do Higher Borrowing Costs Affect Buyers?

When the RBA increases its official cash rate, the cost of borrowing for home loans usually rises too.

Most Australian mortgage products are priced off variable rates or short-term fixed rates that track the cash rate. Even a modest hike of 0.25% doesn’t sound like much in isolation, but it can significantly increase monthly repayments for borrowers on average-sized loans.

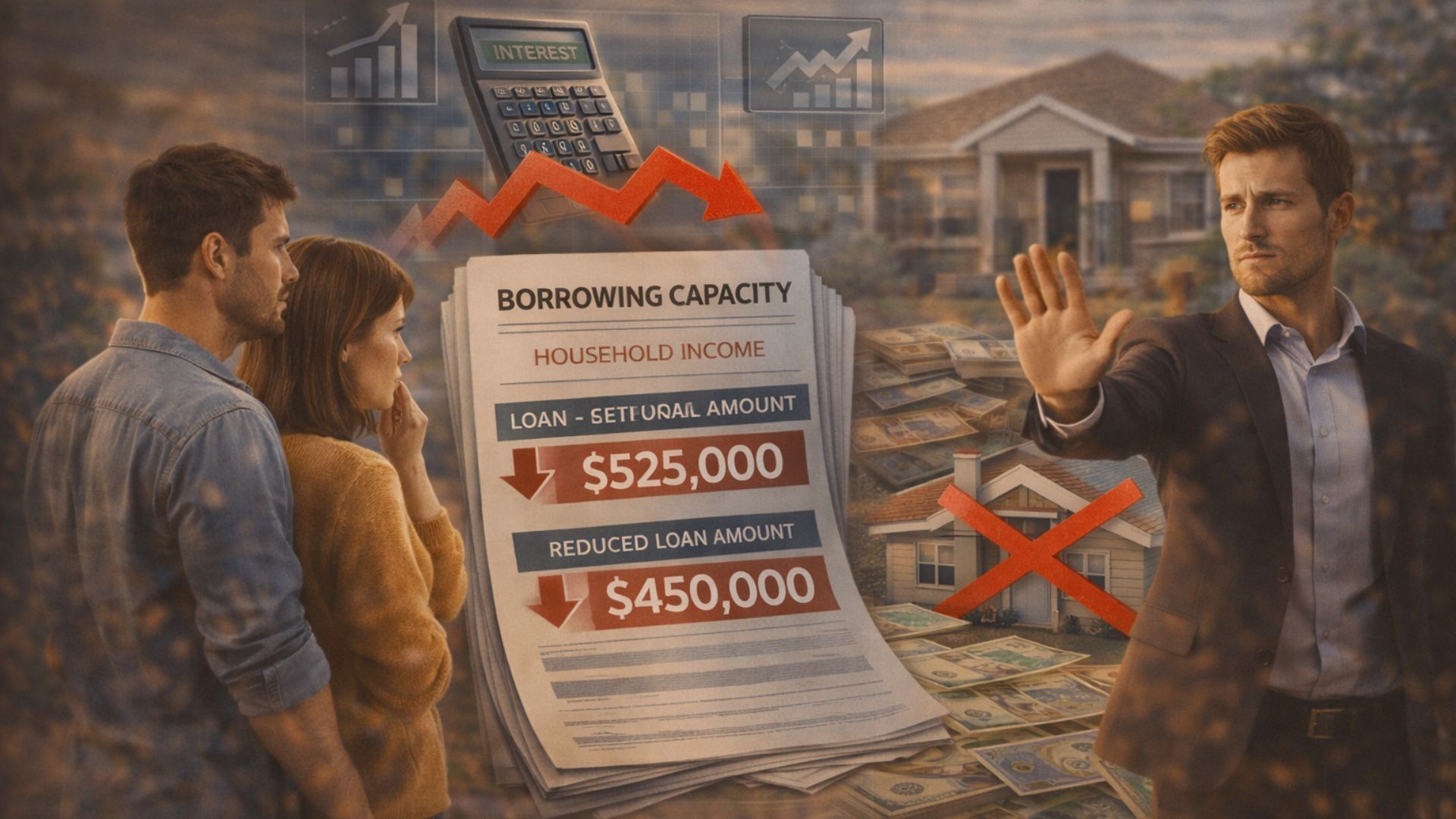

Higher borrowing costs typically translate to reduced serviceability, meaning that buying power for potential property owners will decrease, as lenders will use stricter serviceability tests.

This can directly affect how much Australians can borrow, directly impacting all buyers with first-home buyers feeling the most frustration when trying to enter the market.

For Queensland buyers comparing options, understanding buyers agent Brisbane fees can also help factor professional guidance into the broader purchase budget before borrowing conditions change further.

How Does Buyer Demand Adjust When Rates Rise?

As borrowing capacity compresses, some buyers, especially marginal buyers and first-home buyers, may find their borrowing limits fall.

This means they can no longer afford the same house that they were searching for when rates were lower, and some buyers are expected to need to exit the market altogether.

Reduced borrowing capacity often cools demand at higher price points first, with more buyers demanding the lower price points could in effect squeeze the lower end upwards.

If rates continue to trend upwards, this can slow the pace of property price growth, particularly in highly leveraged and price-sensitive segments.

Markets may still grow, especially in undersupplied areas, but the rate of growth often moderates, especially after a tightening cycle.

Why Do Affordability Pressures Increase?

High inflation and higher rates together exert a two-sided squeeze on households:

- Inflation increases everyday costs, reducing discretionary income.

- Higher interest rates increase mortgage repayments, further tightening budgets.

The combination can dampen buyer enthusiasm. It also tends to favour buyers with stronger financial positions, such as established investors or equity-rich owners, who can weather tighter conditions.

What Are the Implications for Mortgage Holders?

Mortgage holders, especially those on variable-rate loans, are usually the first to feel the effects of a rising cash rate.

A 0.25% rate rise might seem small, but across a large mortgage portfolio it can translate into hundreds of dollars more every month for many households.

Early estimates suggest that if the RBA raises rates, a significant portion of Australian households with mortgages — potentially well over a million — could be pushed into financial stress as repayments absorb a larger share of their income.

For families already stretched by rising living costs, even moderate increases in repayments can force cutbacks in spending, savings, or investment contributions.

Borrowers on fixed rates may have some protection for the duration of their fixed term, but those on variable rates or nearing refinancing will see increases sooner, often within one to three months after a decision by the RBA.

One of the unintended consequences of sudden or unexpected rate rises is that homeowners who assumed rates were headed lower might feel blindsided, and they may need to adjust budgets or refinance at less attractive terms.

How Would Higher Inflation and Rates Impact First-Home Buyers?

The situation is especially challenging for first-home buyers, who already face the toughest hurdles in Australia’s housing system.

Why Does Borrowing Capacity Reduce?

Interest rates directly inform how much banks are willing to lend.

When the cost of servicing debt goes up due to higher rates, the same household income supports a smaller loan amount.

This reduction in borrowing power can price first-home buyers out of markets they could previously consider.

Why Do Higher Deposit Barriers Matter?

With reduced borrowing power, some buyers may also struggle to meet lending criteria for competitive approvals, potentially needing larger deposits to compensate.

In some cases, first-home buyers may delay entry into the market, prolonging their saving goals.

Beyond the numbers, the sentiment of “when will it be affordable?” can affect buyer confidence.

If buyers expect higher costs or see others dropping out of auctions, it can dampen demand further, or at least temporarily.

How Could Property Values Be Affected?

The effects of inflation-related rate rise on property prices aren’t uniform across Australia. They depend on local supply and demand fundamentals, migration patterns, employment trajectories and buyer sentiment.

Will Property Prices Fall or Will Growth Slow?

Even when rates rise, property markets do not suddenly collapse — especially if underlying demand remains strong.

In late 2025 and into early 2026, strong population growth, historically low housing supply, and robust rental markets continue to underpin demand in many capital cities.

Property prices may moderate rather than fall sharply, as buyer demand adjusts to tighter conditions.

Why Could Rental Market Strength Continue?

When interest rates rise, we see continued demand in the rental markets.

The rental markets are driven by population growth and the strong demand can instil investor confidence.

Furthermore, difficulties for first-home buyers to enter the market often means continued strong demand from renters, reinforcing higher rental yields and keeping investors engaged.

What Should Investors and Buyers Know?

Australia’s recent inflation data — with CPI at around 3.8% and rising underlying price pressures — looks set to bring the first RBA rate rise of 2026 as early as February.

For those involved in property markets, here are the key insights:

- Mortgage holders should prepare for higher repayments, particularly if they are on variable rates or nearing refinancing.

- First-home buyers could see borrowing capacity shrink, making it harder to enter the market at current price levels.

- Property values are highly likely not to crash but if rates continue rising, we expect values could moderate as higher borrowing costs dampen demand.

In this environment, savvy investors will continue to monitor credit conditions, lock in competitive finance terms where possible, and pay close attention to local supply-demand dynamics that can cushion markets against broader monetary tightening.

Inflation, interest rates and property values are deeply intertwined, and the RBA’s February decision will be one of the defining economic events shaping the Australian property market in 2026.

Working with the best buyers agent Brisbane can help buyers assess opportunities more strategically when inflation, interest rates, borrowing power, and local market fundamentals are all moving at once.

Final Thoughts

A buyers agent Brisbane can help buyers and investors approach the market with clearer research, stronger due diligence, and a more disciplined strategy during periods of inflation and interest rate uncertainty.

Disclaimer

Aus Property Professionals Pty Ltd retains the copyright in relation to all the information contained on its website and in this guide. This guide, and any content provided in addition, or linked to resources, is general information only and not investment advice.

As everyone’s individual situation is different, we advise individuals to always seek advice from relevant professionals such as legal, financial, accounting, and investing experts.

The intention of this guide is to be used for general information purposes only, in addition to your personal research and due diligence. We do not take any responsibility for any actions taken as a result of this guide as any actions should always be taken with consultation with relevant professionals who take individual circumstances into account.

Past performance doesn’t guarantee future results.

We have compiled the information contained in this guide from online resources, our research, and consultations, and we cannot guarantee the complete accuracy of this information, and we will always reference the resources where the data and information was derived.

****

Thank you for reading our blog on Australia’s Post-Election Property Market. Make sure you head over to our YouTube channel by clicking here to discover more educational insights to level up your property investing including our latest video: Australian Property Market 2025 Forecast.

Disclaimer:

Aus Property Professionals Pty Ltd retains the copyright in relation to all the information contained on its website and in this guide. This guide, and any content provided in addition, or linked to resources, is general information only and not investment advice. As everyone’s individual situation is different, we advise individuals to always seek advice from relevant professionals such as legal, financial, accounting, and investing experts.

The intention of this guide is to be used for general information purposes only, in addition to your personal research and due diligence. We do not take any responsibility for any actions taken as a result of this guide as any actions should always be taken with consultation with relevant professionals who take individual circumstances to account.

Past performance doesn’t guarantee future results.

We have compiled the information contained in this guide from online resources, our research, and consultations, and we cannot guarantee the complete accuracy of this information, and we will always reference the resources where the data and information was derived.

{kind=link}